After an earthquake measuring 7.2 on the Richter scale struck Taiwan on April 3, 2024, people were immediately worried about what impact this might have on Taiwan’s chip production. Even for a well-prepared country like Taiwan, this earthquake is the strongest earthquake in the region in 25 years, which is no small matter. But according to research by TrendForce, the impact on DRAM production will not be significant. The market tracking company believes that Taiwan’s DRAM industry has been basically unaffected, mainly because they have taken strong shock-proof measures.

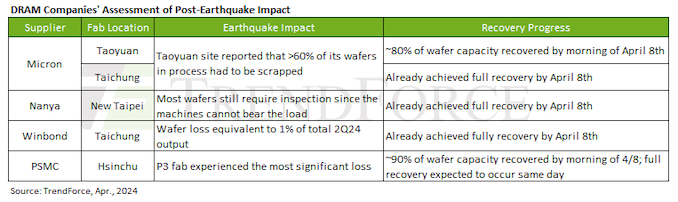

There are four memory manufacturers in Taiwan: Micron is the only member of Taiwan’s “big three” memory manufacturers and operates two wafer fabs. Meanwhile, smaller players include Nanya Technology (which owns one fab), Winbond Electronics (which makes specialty memory in one fab) and PSMC (which makes specialty memory in one factory). The study found that these DRAM producers quickly returned to full operations but had to throw away some wafers. TrendForce said the earthquake is expected to have a small impact on DRAM production in the second quarter, with an impact of only 1%, which is negligible.

In fact, as Micron is ramping up DRAM production for its 1alpha and 1beta nm process technologies, it is increasing memory bit production, which will have a positive impact on commodity DRAM supply in the second quarter of 2025.

After the earthquake, contract and spot DRAM market quotations were temporarily suspended. However, spot market quotations have basically recovered, while contract prices have not yet fully recovered. It is worth noting that Micron and Samsung stopped publishing mobile DRAM quotes immediately after the earthquake and have not provided any updates as of April 8. In contrast, SK Hynix resumed offers to smartphone customers on the day of the earthquake and proposed a more modest price adjustment for mobile DRAM in the second quarter.

TrendForce expects mobile DRAM seasonal contract prices to increase by 3% to 8% in the second quarter. This modest growth is partly due to SK Hynix’s more restrained pricing strategy, which may affect the overall pricing strategy of the industry. According to TrendForce, the impact of the earthquake on server DRAM mainly affected Micron’s advanced manufacturing nodes, which may lead to an increase in the final selling price of Micron’s server DRAM. However, the specific direction of future prices remains to be seen.

Meanwhile, DRAM fabs outside Taiwan were not directly affected by the earthquake. These include Micron’s HBM production line in Hiroshima, Japan, and Samsung and SK Hynix’s HBM production lines in South Korea, all of which are apparently operating as usual.

Overall, the DRAM industry has shown resilience in the face of the earthquake, experiencing minimal disruption and recovering quickly. Ample inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that the modest price increases caused by the earthquake are expected to return to normal soon. The only potential outlier here is DDR3, which is nearing the end of its commercial life and already experiencing declining production volumes.